- 投资101

私募股权与私募股权公共股权:有什么区别?

Private Equity vs Public Equity: an evergreen topic of discussion among investors. Both investment strategies... - 投资101

私募股权与私募股权风险投资:有什么区别?

Navigating the world of finance can often seem like wading through a sea of jargon. Among the many terms... - 投资101

对冲基金与私募股权基金:有什么区别?

Navigating the realm of alternative investments can be a daunting endeavor, especially when it comes to...

市场动态

Linqto 倒闭:对 IPO 前投资者意味着什么

Securities.io 秉持严格的编辑标准,并可能通过审核链接获得报酬。我们并非注册投资顾问,本文亦不构成投资建议。请查看我们的 会员披露.

Linqto On The Brink

Linqto, an investment platform that lets users access shares of privately held companies, filed for bankruptcy on July 8, 2025.

This could put in danger the money of investors that had used Linqto to access shares of private companies, notably the cryptocurrency company Ripple.

The major concern stems from the bankruptcy filing, as well as the declaration by Dan Siciliano, Linqto's CEO:

“Linqto had discovered serious defects in the corporate formation, structure, and operation of the business that raise questions about what customers actually own. The company faces “potentially insurmountable operating challenges.”

To understand what happened, we first need to discuss Linqto's business model and what they seem not to have done as advertised.

Linqto Explained

Private Versus Public Shares

Privately held companies are generally not accessible to most investors. This is because participating in the fundraising for these types of companies is limited to “accredited investors”, a term strictly 由SEC定义 (证券交易委员会)。

Accredited investors must have either a very high income, typically exceeding $200,000/year (with the additional criterion that this income be stable), or a high net worth exceeding $1 million (excluding their primary residence).

Private companies' shares are generally accessible either through participation in funding rounds (an activity often done by private equity firms) or in “secondary markets”, where early investors, founders, or employees can sell some of the shares they own before a public listing.

来源: 林托

This can open access to otherwise uninvestable companies, including Open AI, SpaceX, Kraken, Shield AI, or Ripple, for example. Linqto is one of such secondary marketplaces for private shares.

Linqto’s Business Model

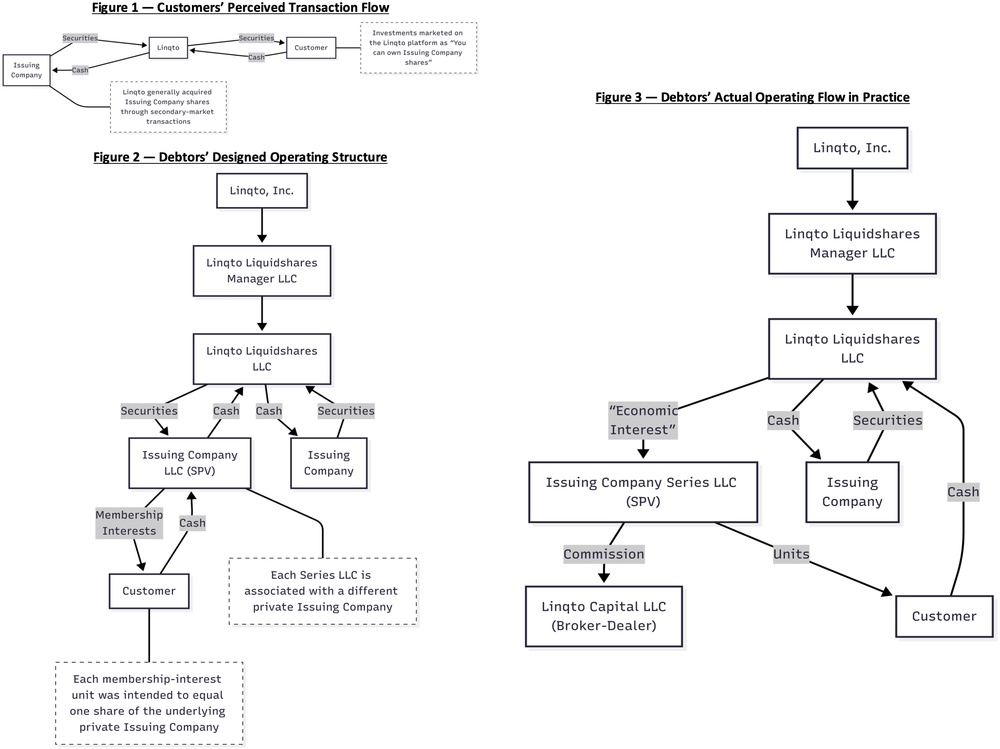

Linqto promised its users 3 main features: instant ownership, direct economic interest in the company associated with the share, and segregation of assets, with the users' assets held in a separate account from Linqto's own assets.

来源: 林托

Linqto aims to invest in mid-to-late-stage companies that it believes will go public or be acquired within the next five years.

So for most investors, the way to “cash-in” from their investment in private companies would be to liquidate their Linqto position after the lockup period following an IPO or acquisition expires, receiving either the cash into their bank account, or the shares in a brokerage account.

Among Linqto's advantages was a very low initial minimum ($1,000), one of the industry’s lowest.

The way Linqto made money was not through fees, as it had no carry, legal, administrative, or profit fees. It instead made money with a purchase premium, reselling the share of private companies it owned at a “reasonable” premium (the actual percentage was undisclosed).

As it turns out now, some of these premiums were rather large, with reports of a 60% markup on Ripple shares, and maybe even higher (anything above 10% is generally flagged as potentially fraudulent by the SEC).

Linqto's model requires it to deploy special purpose vehicles (SPVs), which are a separate company that is bankruptcy remote, allowing users extra protection against a potential Linqto's financial distress.

来源: Bondoro

什么地方出了错?

| 承诺 | 现实 |

|---|---|

| SPV Structure for Asset Protection | No SPVs Created; Assets Pooled |

| Low Purchase Premiums | Markups of 30%–150% Reported |

| Segregation of Customer Assets | No Legal Segregation Found |

Because of the bankruptcy filing, quite a bit of information has been made public.

It appears that Linqto holds $500M worth of shares in 111 companies on behalf of its customers. Some of the most prominent firms that were accessible through Linqto were Stripe, Zipline, Scale AI, Ripple, Patreon, Kraken, and Acorns.

主要问题是 court documents indicate that Linqto never formalized its promised special-purpose vehicle (SPV) structure, did not establish series LLCs, or keep proper records.

来源: Bondoro

So, contrary to the very clear promise made of segregation of assets, still displayed in Linqto's front page, the platform pooled assets with no legal segregation or individual title, according to 托马斯·巴西尔, an attorney who shared his analysis of the case on X.

So this seems to be a clear case of fraud, at least in the sense that the promises made were not delivered upon.

然而,正如所解释的 约翰·E·迪顿, also an attorney, there was no significant fraud in the purchase of shares with users' money. So the money does not appear to have been stolen, but the corporate structure was never as advertised.

Deaton is a Massachusetts attorney and Linqto customer representative, who himself invested nearly half a million dollars into private companies through the platform.

“The other GREAT news is that ALL the shares of companies people invested in (Circle, Ripple, Uphold, Kraken. SpaceX, etc) are present and accounted for. The only caveat to that is that 3% of the shares of Ripple that should be there were sold without people’s knowledge – but the funds related to that sale are there. ”

The legal issues seem to be multiple:

- No SPV setup, contrary to the promise made.

- Excessive markup on some stock and transactions.

- Linqto might have allowed some individuals who were not accredited investors to participate in private share sales, in violation of federal securities regulations.

谁是罪魁祸首?

The initial blame seems to fall to the company's founders, husband and wife Bill and Vicki Sarris, as the decision not to create the SPV structure properly was likely made by them.

Linqto saw a new CEO appointed in March 2025, Daniel Siciliano, who now blames the previous management of the company. With him, the entire executive team was changed, including the Chief Executive Officer of Linqto Capital, the General Counsel of Linqto Capital, the Chief Operating Officer, and the Chief Administrative Officer.

Daniel Siciliano's statement at his appointment indicates he knew some problems were brewing.

“I am excited to be joining Linqto at this inflection moment in the Company’s history.

Despite the urgent need to reset our approach to regulatory compliance, all of us on the new executive leadership team believe that Linqto has the promise to unlock real value.

Most of the new management team hail from Nikkl, a company that has now stopped its operation. It was also active in the private capital market.

Overall, it seems that the company board either knew or recently realized there was a big problem and decided to come clean to the regulator before getting investigated at a point in the future.

“The regulatory issues left unresolved by prior management are critical to address immediately. When we do, we are confident we can deliver on our original mission in a manner that fully complies with all laws and regulations.”

Mike Huskins – Linqto Capital’s newly appointed General Counsel.

The position of the new management, as discussed in the Wall Street Journal, is that they are discovering the issue, which is yet to be clear how true such a statement is, and court proceedings will likely clarify who knew what.

“An internal investigation had uncovered serious securities law violations and practices far beyond minor compliance issues.

Much of what we discovered about the prior business practices at Linqto is disturbing.”

Dan Siciliano – Linqto’s new CEO

What’s Next For Linqto Users?

Most likely, a lengthy legal battle will ensue, with the new management trying to save the company, the old management denying any wrongdoing, and the court having to figure out if the company's board was truly blindsided or actively decided to look the other way.

The bankruptcy itself might be in legal limbo, as Linqto shareholders (the owner of the company, not the users) are apparently looking to fight the bankruptcy proceeding.

A core question is what will happen to the assets and money of the users.

One possibility is that the assets will have to be liquidated, which is probably the worst-case scenario. This is because these shares are very illiquid, as they are not being publicly listed.

So, a forced sale of a bulk of private shares could tank their value, and a court-ordered fire sale would likely not realize the true value of the assets.

A better option would be for the company to restructure, clean its practice during the bankruptcy proceeding, and then re-emerge from bankruptcy. If this is possible and authorized by the courts, it will likely be a way for the private investment of the users without creating unwanted financial losses.

Overall, it seems that Linqto did purchase the shares it said it would, although at an excessive markup, and many of these companies have since grown significantly, meaning that some of the assets might actually be worth a lot more than they appear on the balance sheet.

So there is still a possibility for Linqto users to get their money back, or even make a profit on their investments, depending on how the bankruptcy proceeds and the costs from legal fees.

Where Else To Access Private Shares?

Naturally, the collapse of Linqto brought in the spotlight the risks of investing in private equity markets. Overall, this is a segment that is less transparent, less regulated, and more prone to fraud than the much more scrutinized public markets.

However, this should not deter experienced investors from considering the idea.

First, the situation proves that the sector is actually well-regulated, and potential fraud is being brought to light.

Secondly, the risks should ideally be managed by spreading their investment across multiple platforms, and with the private equity investment making up only a part of the whole investment portfolio.

如果您符合要求并且能够承受风险,以下几个平台可以提供 IPO 前机会:

打造全球:最大的私募股票市场之一,提供 SpaceX、Stripe 和 Databricks 等后期初创公司的股票。最低投资额通常在 100,000 万美元左右。

净资产:一个热门平台,允许合格投资者以低至 5,000 美元的最低投资额入股私人公司。过去曾服务过 Discord 和 UiPath 等公司。

雨人证券:一家提供全方位服务的经纪商,帮助寻找和协商私人股票销售,包括 OpenAI、Stripe 和 Palantir 等公司的机会。

蜂巢:一个较新的平台,为数百家私营公司提供实时买卖报价。透明且费用低廉,最低交易额约为 25,000 美元。

MicroVentures:通过特殊目的载体(SPV)提供对后期公司的集中访问权,包括过去对 SpaceX 和 Instacart 的投资。

股票蜂:允许投资者为初创公司员工股票期权的行使提供资金,通常以折扣价,最低金额约为 10,000 美元。

增强:一个数字优先的市场,显示首次公开募股前股票的实时定价,针对精通技术的投资者并提供较低的交易费用。

StartEngine 私人:该平台于2023年底上线,为合格投资者提供参与后期风险投资公司D类上市的渠道。上线后的前九个月,该平台创造了16.5万美元的收入,平均投资额约为32,000万美元。

Are Pre-IPO Investments at Risk After Linqto?

The situation with Linqto should not directly affect the company whose shares it owns for the moment.

At worst, it could cause a temporary excess of supply in the secondary private market, and only if the court were to order an instant and total liquidation of all Linqto assets, irrespective of the price that could be obtained for them.

The reputational damage should also be limited, with the most exposed firms like Ripple already taking preventive actions.

“Understandably, there have been many questions from those who believed they were buying Ripple shares from Linqto, and what happens next.

What we know from our records is Linqto owns 4.7 million shares of Ripple, solely purchased on the secondary market from other Ripple shareholders (never directly from Ripple).”

Brad Garlinghouse reiterated that the firm itself never sold shares to Linqto or had any formal business relationship with the platform.

结语

Linqto's situation is rather unfortunate, and hopefully, it should not cause a loss of money for its users who trusted the platform.

This however should not change how the overall, much larger field of private equity investing is perceived. At least not more than past scandals in public markets (Enron, subprimes) have affected the long-term investability of public markets.

Investing is an inherently risky activity. A more illiquid market, like private equity, is even more so. This is nevertheless an increasingly attractive sector, as the world's leading companies like OpenAI or SpaceX are delaying IPO much more today than equivalent companies in past decades.

With a lot of money flowing into the sector, the temptation for bad actors to misrepresent their actions and defraud investors grows. This is why going for platforms that are well established and well audited is maybe preferable, as well as not using only one platform.

Investors should also pay attention to the transparency of the business model, with well-understood fees sometimes preferable to more opaque no-fees approaches.

{kind=link}